Apple 3.0

For more, please login or subscribe

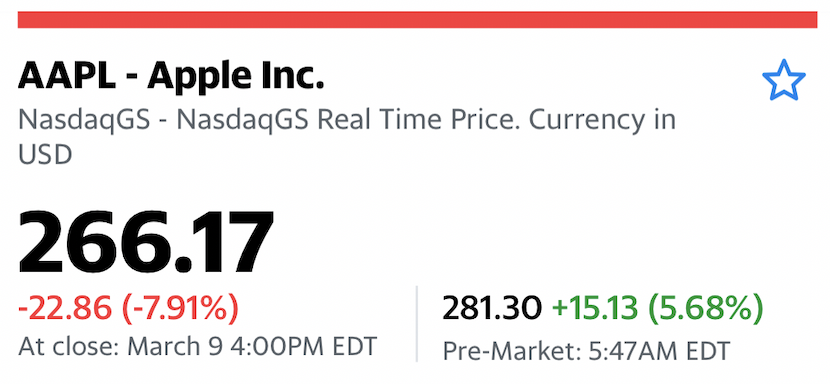

Previous Post The good news about Apple's 6.54% pummeling...

Next Post Disinfectant wipes are OK for users, but not for Apple Geniuses

6 years ago

6 years ago