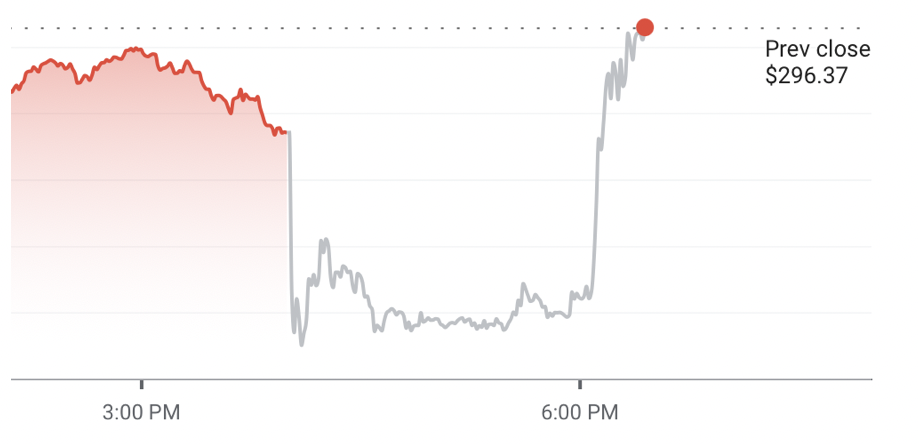

"The Strong Cloud Guidance Heard Around the World; Cloud Growth Not Slowing!!"For more, please login or subscribe