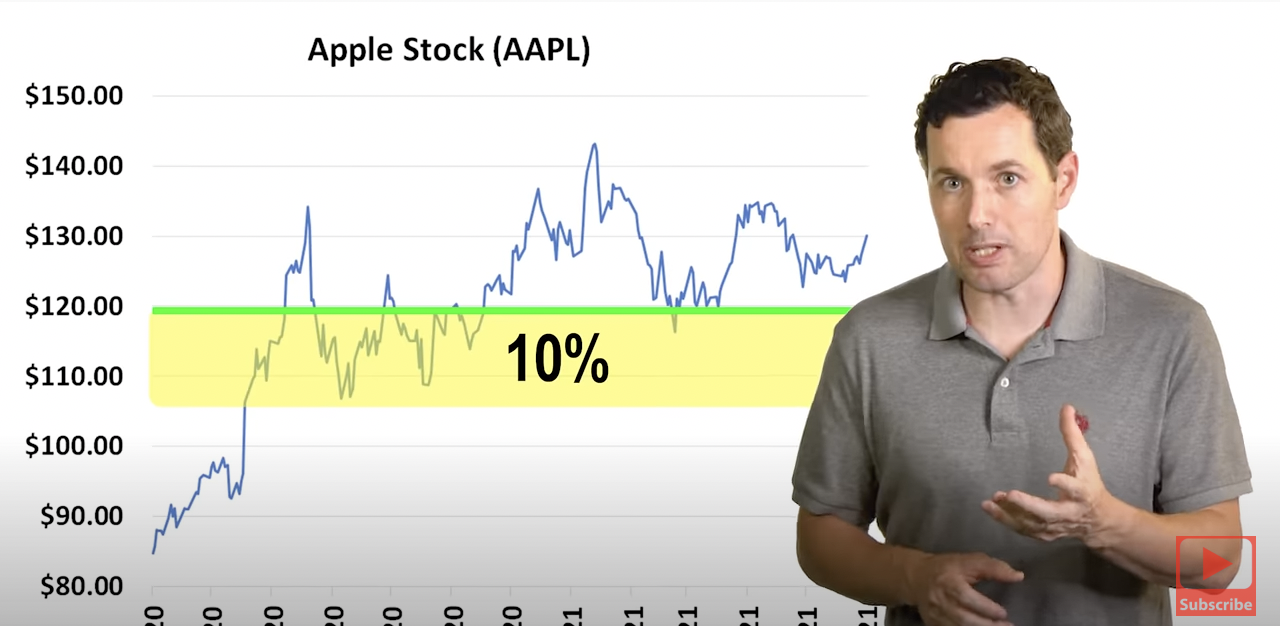

And the end of a 9-minute discounted cash flow tutorial JWC's Jimmy Copell sets his buy point 10% lower.For more, please login or subscribe

5 years ago

5 years ago