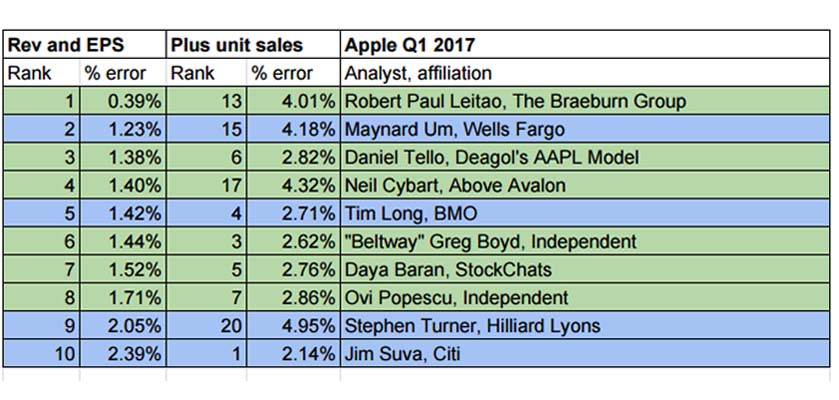

Independent Apple analysts this quarter took six out of 10 top spots. When Apple beats expectations, the congenitally bullish independent analysts tend to shine, throwing shade on…

Philip Elmer-DeWitt has been covering Apple since 1983 — mostly for Time Magazine (28 years), later for Fortune (9 years), where he wrote a daily blog called Apple 2.0. [Read more.]

9 years ago

9 years ago

You must be logged in to post a comment.