This is why Apple wishes it were an Internet company

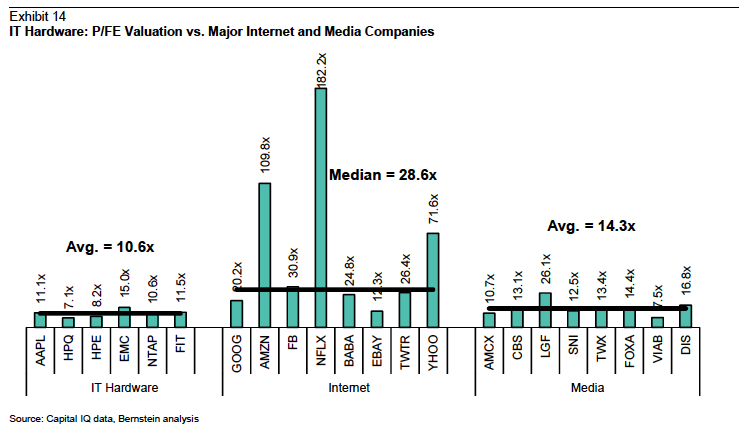

It might be valued less like Hewlett Packard or Time Warner and more like Facebook or Yahoo. This bar chart comes courtesy of Bernstein's Toni Sacconaghi, who sees…

Philip Elmer-DeWitt has been covering Apple since 1983 — mostly for Time Magazine (28 years), later for Fortune (9 years), where he wrote a daily blog called Apple 2.0. [Read more.]

10 years ago

10 years ago